Ever applied for a credit card and suddenly your credit score dropped a few points? You’re not alone, and the culprit is often a hard inquiry.

Understanding hard inquiry meaning is crucial in today’s credit-driven world.

Whether you’re applying for a loan, financing a phone, or just exploring credit options, these checks can quietly impact your financial profile.

Here’s the thing: not all credit checks are created equal. Some are harmless, while others, like hard inquiries, can leave a mark.

In this guide (updated for 2026), you’ll learn exactly what a hard inquiry is, how it works, when it matters, and how to manage it smartly.

We’ll break it down in plain English, no confusing finance jargon.

What Does “Hard Inquiry” Mean?

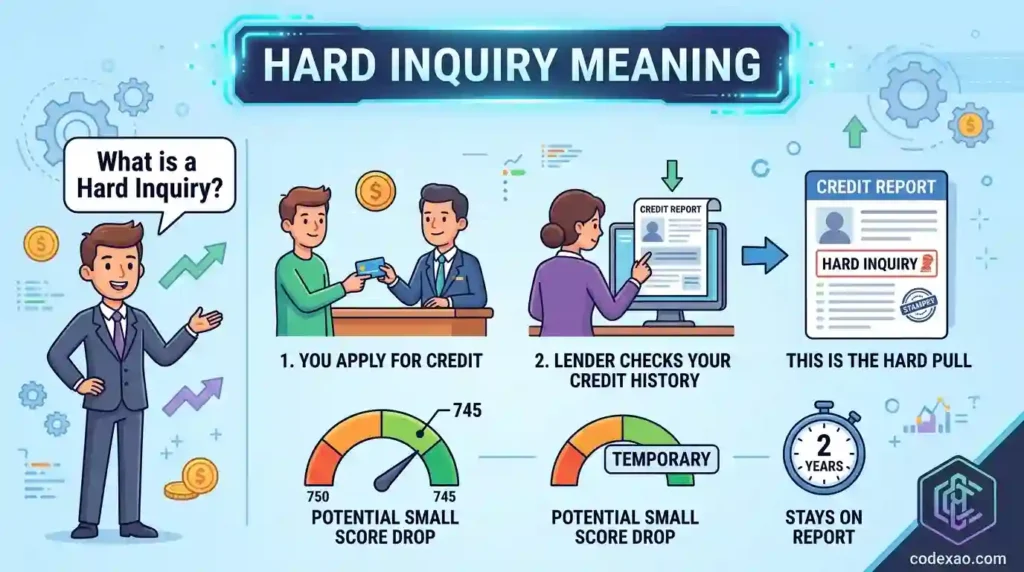

A hard inquiry (also called a hard credit check) happens when a lender reviews your credit report after you apply for credit.

This usually occurs when you apply for:

- Credit cards

- Personal loans

- Mortgages

- Car financing

🔎 Quick Answer:

A hard inquiry is a formal credit check by a lender that may slightly lower your credit score and stays on your report for up to two years.

Origin & Evolution

The term comes from the credit reporting industry, where inquiries are categorized as either “hard” or “soft” based on their impact. As digital lending grew in the 2000s, hard inquiries became more visible to everyday users through apps and credit monitoring tools.

Today, people track them closely because even small score changes can affect approvals.

Pronunciation

“Hard in-kwy-uh-ree”

How to Use “Hard Inquiry” Correctly in Texts & Chat

Unlike slang, “hard inquiry” is more of a financial term, but it still pops up in casual conversations, especially online.

Tone & Context

- Neutral and informational

- Often used in finance discussions

- Sometimes used casually when talking about credit scores

Platform Usage

- WhatsApp: “I got a hard inquiry after applying for that loan 😬”

- Instagram DM: “Does this app do a hard inquiry or soft one?”

- Twitter/X: “Too many hard inquiries can mess up your credit score”

- Reddit/Discord: Common in finance threads

When to Use It

✅ Talking about credit applications

✅ Discussing credit score drops

✅ Asking about loan approvals

When NOT to Use It

❌ Casual chats unrelated to finance

❌ Professional emails without explanation (use full context instead)

Formatting Tips

- Usually lowercase: hard inquiry

- Often paired with terms like “credit score,” “loan,” or “application”

- Emoji combos: 😬📉💳

Real Conversation Examples Using “Hard Inquiry”

1. Between Friends

A: “Why did your credit score drop?”

B: “I applied for two cards. Each one caused a hard inquiry.”

Shows cause-and-effect in a casual tone.

2. Dating Scenario

A: “You’re really into finance, huh?”

B: “Yeah, I even avoid unnecessary hard inquiries 😂”

Adds humor while showing awareness.

3. Family Discussion

Parent: “Why not apply for another loan?”

You: “Too many hard inquiries can hurt my chances.”

Used to explain financial caution.

4. Work Chat

Colleague: “Should I apply for this credit card?”

You: “Check if it triggers a hard inquiry first.”

Helpful and advisory tone.

5. Gaming/Online Chat

User: “My score dropped randomly!”

Reply: “Probably a hard inquiry from something you applied for.”

Quick explanation in a fast-paced chat.

Common Mistakes & Misunderstandings

1. Confusing Hard vs Soft Inquiry

Many think all credit checks hurt their score. Not true. Only hard inquiries have an impact.

2. Thinking It’s Permanent Damage

A hard inquiry only affects your score temporarily. The impact fades within months.

3. Ignoring Multiple Applications

Applying for many loans quickly can stack hard inquiries, this can signal risk to lenders.

Generational Confusion

- Gen Z: More aware due to fintech apps

- Older users: Often unaware of inquiry types

Cultural Differences

In some regions, people rarely check credit reports, so terms like “hard inquiry” feel unfamiliar.

How to Clarify

If someone doesn’t understand, say:

“It’s just a credit check that can slightly lower your score.”

“Hard Inquiry” Across Different Platforms & Demographics

Gen Z vs Millennials

- Gen Z: Tracks inquiries via apps like credit trackers

- Millennials: More cautious due to past financial experiences

Platform Trends

- TikTok: Financial influencers explain credit tips

- Reddit: Deep discussions on credit strategies

- Instagram: Bite-sized financial advice

Formality

- Informal but financial

- Safe for work (SFW)

- Common in money-related discussions

Popularity Spike

The term gained traction as more people started using credit monitoring apps and fintech platforms.

Related Slang, Abbreviations & Alternatives

| Term | Meaning |

|---|---|

| Soft Inquiry | Credit check with no score impact |

| Credit Score | Numerical rating of creditworthiness |

| Pre-Approval | Initial credit check (usually soft) |

| FICO Score | Common credit scoring model |

| Credit Report | Detailed financial history |

| APR | Annual Percentage Rate |

| Debt-to-Income Ratio | Measures debt vs income |

| Credit Utilization | Credit used vs limit |

| Loan Application | Request for borrowed funds |

FAQs:

What is a hard inquiry vs soft inquiry?

A hard inquiry happens when you apply for credit and can lower your score slightly. A soft inquiry occurs during background checks or pre-approvals and does not affect your credit score.

How many hard inquiries are too many?

Generally, more than 3–5 hard inquiries in a short period may raise concerns for lenders. It can signal that you’re actively seeking credit, which may appear risky.

Can I remove a hard inquiry from my credit report?

You can only remove it if it’s incorrect or unauthorized. Otherwise, it stays on your report for up to two years.

Do hard inquiries affect loan approval?

Yes, multiple hard inquiries can impact approval decisions, especially if they appear within a short time frame.

How can I avoid hard inquiries?

Limit unnecessary credit applications and check if lenders offer pre-qualification with a soft inquiry before applying.

Conclusion:

Understanding hard inquiry meaning gives you a real advantage when managing your credit. It’s not just a technical term, it directly affects your financial opportunities.

The key takeaway? Hard inquiries aren’t dangerous, but too many in a short time can be.

Be intentional. Apply for credit wisely. And always check whether it’s a soft or hard inquiry before hitting that “Apply” button.

Got a question about credit terms or slang? Drop it below, and let’s decode it together.

Hi, I’m Isabella Brown, the voice behind Codexao.com, where meanings aren’t just explained, they’re made easy to understand.

I’ve always been fascinated by how words shape the way we think, speak, and connect. But let’s be honest—most definitions out there feel confusing, outdated, or just plain boring.

That’s exactly why I created Codexao. Here, I break down words, slang, and modern expressions into simple, clear meanings you can actually use in real life.